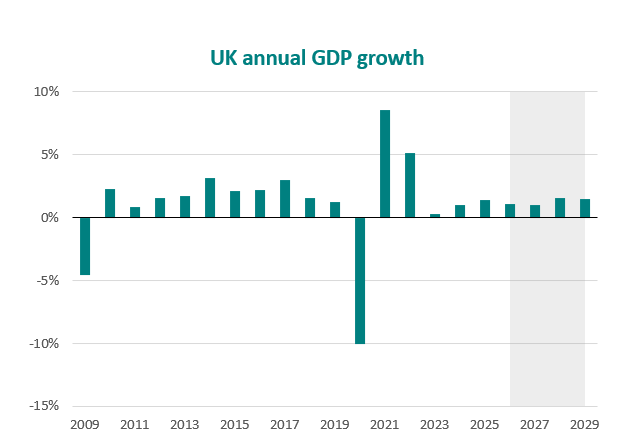

UK real GDP grew by 0.6% in Q1 2026, a stronger start to the year than anticipated, but potentially a high-water mark given the headwinds caused by escalating conflict in the Middle East. The disruption, particularly to global energy supply, is expected to weigh significantly on growth over the rest of the year, as rising input costs are increasingly passed onto consumers, putting pressure on discretionary spending.

The UK’s labour market troubles persist, with the unemployment rate still elevated in Q1 2026 and job vacancies falling. Rising slack in the job market is contributing to a deceleration in earnings growth, placing pressure on real incomes and households' spending power.

Headline CPI inflation came in at 3.1% in Q1 and is expected to have eased in Q2. The Ofgem price cap, set before the start of the ongoing energy crisis, will temporarily insulate UK consumers from significant gas and electricity inflation. That said, inflation is forecast to be remain elevated in Q2 compared to pre-war forecasts.

The conflict in Iran is expected to weigh on near-term growth prospects in both the Eurozone and the United States, as renewed inflationary pressures constrain the ability of the European Central Bank and the Federal Reserve to adopt a more expansionary monetary policy stance. China posted robust growth in Q1, but early estimates point to Iran-related disruption weighing heavily on economic output in Q2.

London, the North East, and the South East are projected to be the fastest-growing regions in the UK this year, while the devolved nations and Yorkshire and the Humber are expected to grow at the slowest pace.

• UK growth prospects

• The labour market

• Inflation and interest rates

• Global growth prospects

• Regional prospects

• Topical economic issues