The December edition of the YouGov/Cebr Consumer Confidence Index released last week saw consumers grow less pessimistic with a 1.0 point improvement in the overall confidence score, which now stands at 95.9. The rise was driven by gains in the short-term (+3.3) and forward-looking (+8.8) household finance measures. Given the ongoing cost-of-living pressures and corresponding erosion of disposable incomes (The Asda Income tracker produced by Cebr shows disposable incomes contracting 11.4% year-on-year in November[1]), the news that consumer confidence is recovering came as quite the surprise.

Rising confidence in the face of falling disposable incomes suggests that consumers may have found ways to maintain their lifestyles despite spending more on essentials. One way to achieve this would be to dip into Covid savings, assuming there are any left. We define Covid savings as the additional savings set aside by households in 2020 and 2021 as a result of limited consumption opportunities, with figures from the ONS suggesting that this equated to £5,200[2] for the average household.

In the meantime, households have seen a stark fall in their spending power. Cebr’s Income Tracker, produced in collaboration with Asda, showed that weekly spending power for the average household dropped significantly in 2022, dipping to a low of £201 in October 2022, having averaged £243 across 2021. Combining these figures, Cebr estimates that the typical household has drawn down £1,500 of their Covid savings simply to maintain their standard of living from 2021. In addition, households have spent a further £900 on non-essential goods and services that were unavailable for much of the pandemic, such as holidays and hospitality. In total then, the average household has spent £2,400 of the savings they accrued during the pandemic, equivalent to 47% of the total.

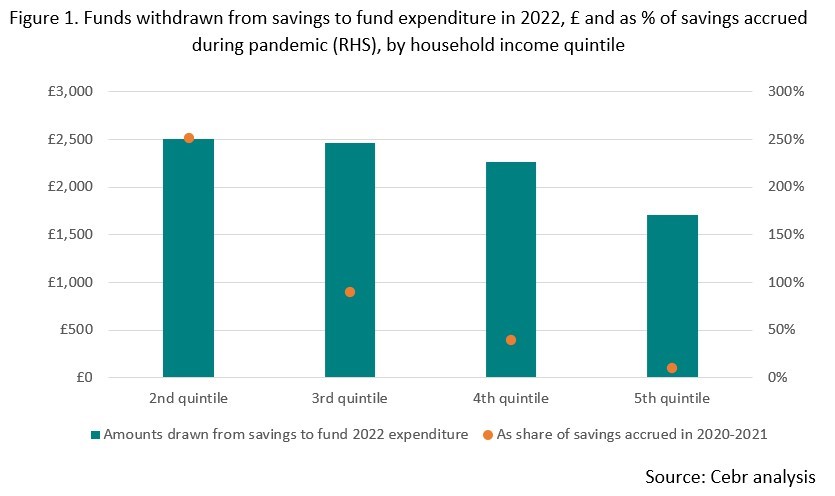

There is stark variation when looking at different household demographics. Our regular work on discretionary incomes shows that those in the first income quintile, i.e., the lowest earning fifth of households, are unable to save, with the cost of essentials taking up all of their income. This was the case even during the pandemic period. Households in the second quintile were able to accrue some additional savings during the pandemic period, but we find that they have had to draw down a larger amount than the average household, reflecting their exposure to price pressures at present. Second quintile households parted with £1,900 to maintain their standard of living at 2021 levels and spent a further £600 on non-essentials that were unavailable during the pandemic. Collectively, this has exhausted the savings they built up due to Covid. Meanwhile, though the top 20% of households have drawn down on their pandemic savings, this amount is much smaller than average, at £1,700. Unlike poorer households, the drawdown in this case has predominantly been driven by increased expenditure on non-essentials, rather than spending to maintain their everyday living standards.

The ability (or lack thereof) to dip into Covid savings as a means of maintaining living standards amidst the cost-of-living crisis goes some way toward explaining varying levels of confidence between consumers at different points on the income scale.

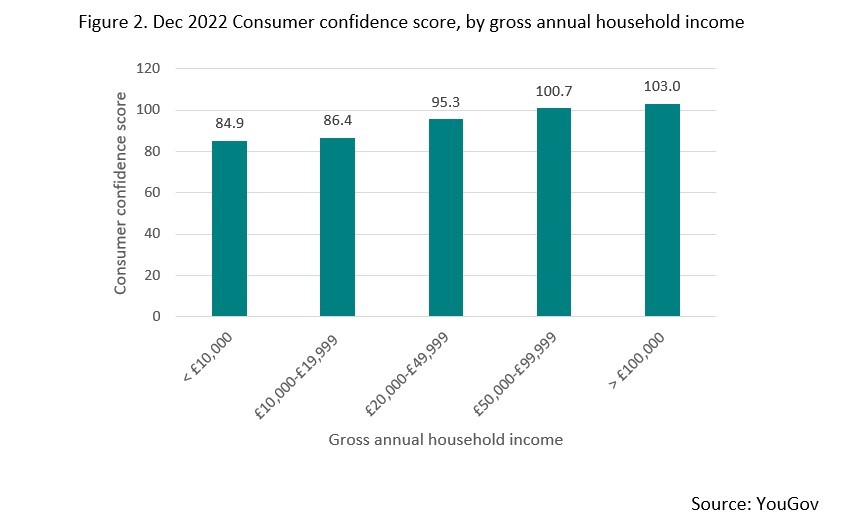

The poorest households (those with a gross annual household income of less than £10,000) recorded a confidence score of just 84.9 in December – 11 points below the national average and a whopping 18.1 points below the confidence level for the highest earning households.

Our analysis highlights just how unequally the ongoing cost-of-living crisis is impacting households along the income scale. Not only are poorer households being hit the hardest because of the rising cost of essentials, which make up a higher share of their expenditure, but they are also the ones that are least able to offset this shock by dipping into their Covid savings. On the other hand, wealthier households have been better able to maintain their living standards, as even more than a year after all significant Covid rules were lifted they still enjoy the benefit of Covid savings, having spent just 10.5% of the accumulated sum.

While inflation may be finally taking a turn for the better, Cebr expects CPI to stand at nearly three times its target level by the end of 2023. While many will feel the squeeze, the poorest households will bear the brunt of the crisis, making it unsurprising that their confidence levels are so far behind the rest.

[1] https://corporate.asda.com/media-library/document/asda-income-tracker-december-2022/_proxyDocument?id=00000185-2983-dde7-abcd-6b87e30d0000

[2] Cebr analysis of ONS bulletin on forced saving during the Covid-19 pandemic

For more information contact:

Nina Skero, Chief Executive Email nskero@cebr.com,

Phone: 020 7324 2876

Sam Miley, Senior Economist Email smiley@cebr.com

Phone 020 7324 2874

Cebr is an independent London-based economic consultancy specialising in economic impact assessment, macroeconomic forecasting and thought leadership. For more information on this report, or if you are interested in commissioning research with Cebr, please contact us using our enquiries page.