Policy changes at the Autumn Budget have further added to a trend: the cost of university is being shifted from government to graduates. Many of those on repayment plans face a steadily rising mountain of debt, to which they will dedicate a share of their monthly salaries for most of their working lives. We estimate that the average 2022 graduate will spend £9,300 more servicing student debts as a result of the temporary freeze in repayment thresholds. From a wider perspective, though these changes are unlikely to bring short-term impacts, there is a risk that this mounting trend could disincentivise university entry in the coming years.

The announcement in the Autumn Budget to freeze repayment thresholds for graduates making loan repayments under Plan 2 until 2029 is another example of a stealth policy. It increases both the number of graduates making payments and the amount they repay each month, as inflation drives up nominal wages.

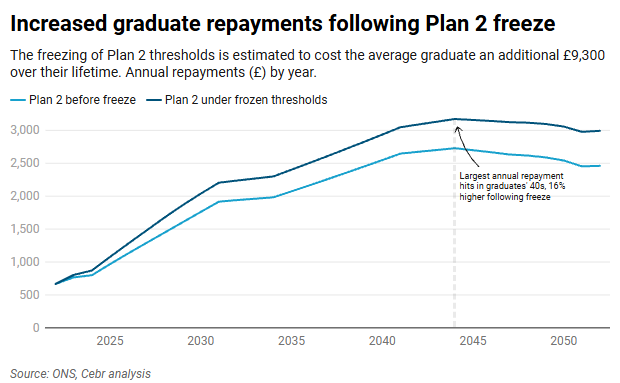

The impact on any given graduate is not insignificant. Indeed, we estimate that the average student graduating university in 2022 is now expected to contribute approximately £69,300 in repayments until their outstanding balance is cancelled. This is equivalent to 3.4% of their total earnings up to the loan cancellation date. Had the repayment thresholds not been frozen, we estimate graduates would have saved approximately £9,300 over their lifetime.

Looking at the impact across different life stages, repayments will peak when graduates are most likely to be earning above the average – in their 40s. This is the point at which the largest annual repayment is expected to hit those with university degrees, higher now by £444 (16%) per year than if thresholds had not been frozen.

These changes to loans affect those who have already been to university. As such, in themselves they will do little to disincentivise future attendees. However, the wider trend of shifting higher education costs from government to graduate may well do.

At the moment, graduates continue to outperform others who did not go to university. In 2024, for instance median graduate earnings stood at £42,000, surpassing those of non-graduates by £12,500. Yet, students exiting university now may feel uncertain about the existence of this ‘graduate premium’, particularly if they are finding difficulties entering the labour market in the first place. Unemployment in the UK has been steadily ticking up since the end of the pandemic, recently reaching its five-year peak, while vacancies have fallen significantly. Youth unemployment also reached a 10-year high recently. In this context of relative economic malaise, student loan concerns may compound with broader pessimism to question the returns from the university system.

Still, the effects of these changes on the wider economy are unlikely to be felt in the short term. Under the repayment and interest rate threshold freezes, the OBR estimates government cash receipts will increase by £0.4 billion a year in the medium term and a one-off reduction in borrowing in 2026-27 of £5.6 billion. As spending on loans is reduced, the government counts with more funds, now freed up to be directed elsewhere and stimulate growth.

It is possible, additionally, that the money will work harder under government hands than it would have in those of graduates. Facing financial pressure and economic uncertainty, younger generations may be more likely to save respective to their predecessors in preparation for future financial obligations. If graduates are more likely to save rather than spend additional disposable income, they will generate less economic stimuli than the government will from funding expenditure through loan repayments.

In the long term, however, the government ought not to over-ask of its graduates or risk disrupting the UK labour market. The UK has long been a service-based economy, with many roles reliant on a stream of graduates. Thinking about the future labour market structure may even exacerbate this, with data and tech roles expected to be amongst the fastest growing in the coming years. To capitalise off these opportunities, the UK will require talent that can take on the roles.

Overall, a balance ought to be maintained between reduced government spending on education and the need to fund competitive universities which can bolster the UK’s human capital. While the student loan system by itself is unlikely to jeopardise the future of higher education, an unfavourable context for graduates can heighten perceived fears around job prospects. To the extent that fear shapes decisions that steer the economy, government cannot afford to ignore it.

Beatriz Rilo, Senior Economist, brilo@cebr.com, 020 7324 2873

Cebr’s next Forecasting Eye will be released on 20th March.