Introduction

One issue affecting the effectiveness of sanctions and the corresponding response in the currency and other markets is how they affect Russian living standards.

This short note models one scenario to get a sense of how quickly the combination of sanctions, rising commodity prices and the fall in the ruble will affect Russian living standards.

The modelling is aimed to be consistent with the Cebr estimate that sanctions on Russia will reduce Russian GDP by 14%[1].

The latest data from Rosstat[2] shows that prices have risen by 2.2% and 2.1% in the first two weeks of March respectively. The Russian February CPI was already up 9.2% on a year earlier, more than twice the official inflation target of 4%.

The most recent data shows Russian wages up by 3.6% compared with a year earlier but President Putin has vowed to prevent drops in living standards claiming that he will raise the minimum wage and benefits to compensate for rising costs[3].

Key results

What is different this time from 2014-15 when the economy was also hit by sanctions is that the ruble is falling at the same time as commodity prices have also risen sharply. So the push on inflation is rather greater and the impact on living standards correspondingly so.

The key elements of our forecast are:

- Russian inflation likely to hit 30% in early 2023

- Real wages to fall by 18% over the next 12 months

- Real wages to be reduced by 25.7% to December 2024.

Assumptions

Obviously there is a wide range of possible assumptions. This analysis makes some central estimates to be applied as assumptions:

- The Bank of Russia follows counterinflationary policies to stabilise the ruble but is unable to stabilise the cost of living initially;

- Wages are raised at an annual rate of 10% until inflation falls below that level

- We have assumed that oil, gas, metals, fertilisers and food prices are roughly at their spot prices at the beginning of March – the same assumptions in Cebr’s analysis of the impact of the invasion of Ukraine on the UK economy[4].

Methodology

We have forecast Russian inflation by applying Russian CPI weights to the price rises which we had assumed for the UK, but adjusted for the fall in the ruble.

In 2013-15 the ruble fell by 48% as a result of sanctions and other actions. A consequence was that annual inflation rose from 6.7% in 2013 to 15.5% in 2015[5]. A recent note by the Bank of Russia observed that 44% of the consumer basket is imported[6] and therefore affected directly by the value of the ruble (some domestic prices are also). Our model forecasts domestic inflation and imported inflation using 0.44 as the weight for imported inflation.

We have calculated the Russian CPI basket based on the available data. A key feature is the prominence of food: the latest index has a weight of 33.1% for food[7] and about 6% for energy and heating. Other important categories are transport (14 percent); clothing and footwear (11 percent); housing, water, electricity, gas and other fuels (11 percent); recreation and cultural activities (6 percent), alcoholic beverages and tobacco products (6 percent) and household appliances (6 percent). Health, communication, education, hotels, restaurants and other goods and services account for the remaining 16 percent of total weight[8].

The forecasts

CPI

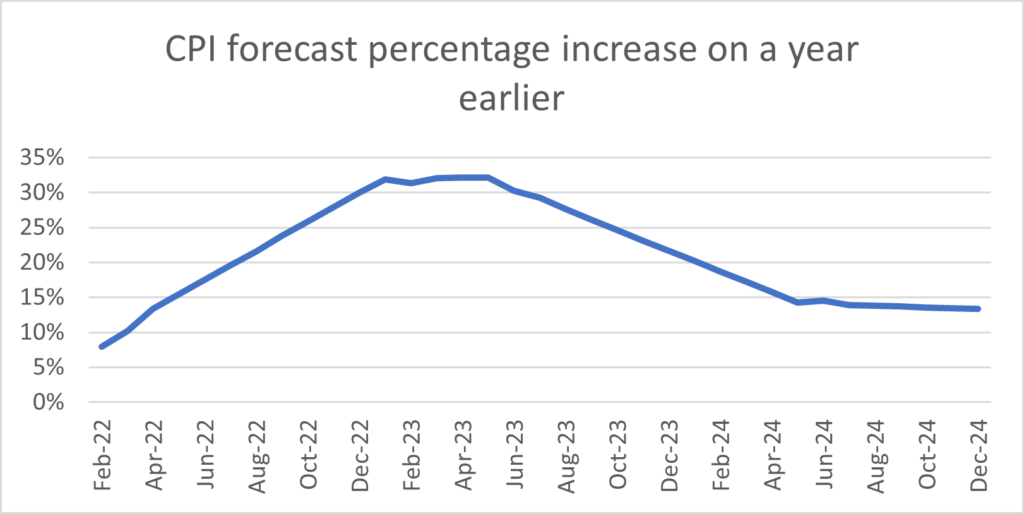

Making these somewhat crude assumptions and assuming a distributed lag of 9 months gives the data to make it possible to forecast the Russian cost of living. The forecasts are shown in Figure 1.

Figure 1

They show inflation rising gradually to just over 30% early next year, staying there for about 7 months and then falling gradually to about 15% in Spring 2024 before edging slightly lower in the rest of 2024.

Of course part of the impact of sanctions means that certain goods are unobtainable except on the black market. We have not taken this into account for these forecasts.

The standard of living

Together with our wage assumptions we have made an estimate of what this inflation forecast means for the standard of living. Technically we have defined the standard of living as the real value of wages, ie wages deflated by the CPI.

The results are shown in Figure 2.

This shows wages falling quite sharply initially – by 18% in the year to February 2023 before falling very much more slowly. They end down a quarter.

Figure 2 Russian real wages

Conclusions

These results show that the combined effects of sanctions, the fall in the ruble and the rises in commodity prices associated with the Russian invasion of Ukraine on real living standards in Russia are severe. Could the Russian government do anything to mitigate this very severe impact? There is some scope. Many prices in Russia are state controlled or subsidised. A World Bank assessment in 2019 estimated that energy subsidies alone in Russia in that year amounted to 1.4% of GDP[9]. With a budget surplus from high oil revenues there is scope for subsidies to be increased, though at the expense of increasing market distortions. And presumably other products could also be subsidised. The extent of the subsidy would limit the squeeze on living standards.

And we have assumed that wages and benefit increases are limited by the weakness of demand for labour to 10% per annum. Again wages could be increased more, though to prevent Russia becoming uncompetitive these would probably have to be matched by a fall in the value of the ruble. This fall would itself be inflationary.

The scale of the budget surplus[10], however means that the scope for alleviating more than half the squeeze on living standards is limited and even this could probably only be maintained for about a year.

So the squeeze on Russian living standards is likely to be severe and will be hard to offset.

Douglas McWilliams, Deputy Chairman, Cebr

London, March 2022

[1] https://cebr.com/reports/financial-sanctions-set-to-cause-a-14-hit-to-russian-gdp-by-2023-if-the-west-can-stomach-the-costs-of-throttling-energy-exports/

[2] https://rosstat.gov.ru/storage/mediabank/41_16-03-2022.htm

[3] https://www.ft.com/content/4a3c500f-708c-4879-b1c7-ecd1be0f99a5

[4] https://cebr.com/wp-content/uploads/2022/03/Cost-of-Russian-invasion-of-Ukraine-for-the-UK-economy.pdf

[5] All data in this section is from the IMF World Economic Outlook database, October 2021 edition

[6] Bank of Russia: About Inflation https://www.cbr.ru/eng/dkp/about_inflation/

[7] Table RU.IA027: Consumer Price Index: Weights

[8] https://tradingeconomics.com/russia/inflation-cpi

[9]Energy Subsidies in Russia: Size, Impact, and Potential for Reform World Bank 2019

[10] The IMF forecast for 2022 in October 2021 was a government budget surplus of 0.2% of GDP